| Ø | Double click the Runname editing box and type a name for the dataset, e.g., optimize. |

| Ø | Click on the Optimization button  on the Toolbar. The Payoff dialog opens. on the Toolbar. The Payoff dialog opens. |

| Ø | Click on the Add button. Select the option button for Policy. Click on the Sel button next to Variable and select profit from the list, then click OK to the variable selection dialog (or just type profit into the editing box). |

| Ø | Click on the Weight editing box and type the number 1. Click on the button Add Editing. |

Positive weights designate more is good (more profits); negative weights designate more is bad. If more than one parameter set in the payoff, you need to balance (or weight) your parameters appropriately. See the calibration example earlier in this chapter or Optimization in the Reference Guide for more information on setting up payoffs.

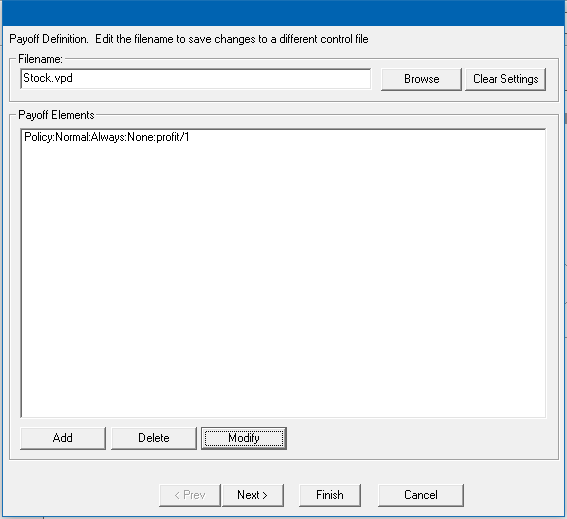

Your Payoff Setup dialog should appear as below:

| Ø | Click Next. |

Note that policy optimizations maximize the integral of the payoff. Thus using profit in the payoff is the same as maximizing Cumulative Payoff at the end of the simulation.